Doctolib’s Profitability Issues

A positive net profit is expected this year. Is that a good sign?

I recently read several articles announcing that Doctolib has reached €348 million in annual recurring revenue by 2024, which would represent a 22.5% growth compared to its 2023 ARR.

Over the past five years, Doctolib’s growth has also averaged 22.5% per year, which indicates steady expansion.

France remains Doctolib’s primary market, representing 80% of its 2024 ARR (or approximately €278 million). Germany, meanwhile, is in second place, with 7% of its ARR (approximately €59 million), 25 million registered patients, and 100,000 healthcare professionals. Italy represents approximately 2.6% of its ARR (approximately €9 million). Doctolib’s European expansion plans are clear, even if profitability questions remain.

Doctolib has reduced its operating loss by 38%, from €87.1 million in 2023 to €53.8 million in 2024. Profitability is expected this year. But will it be a typical SaaS break-even event ?

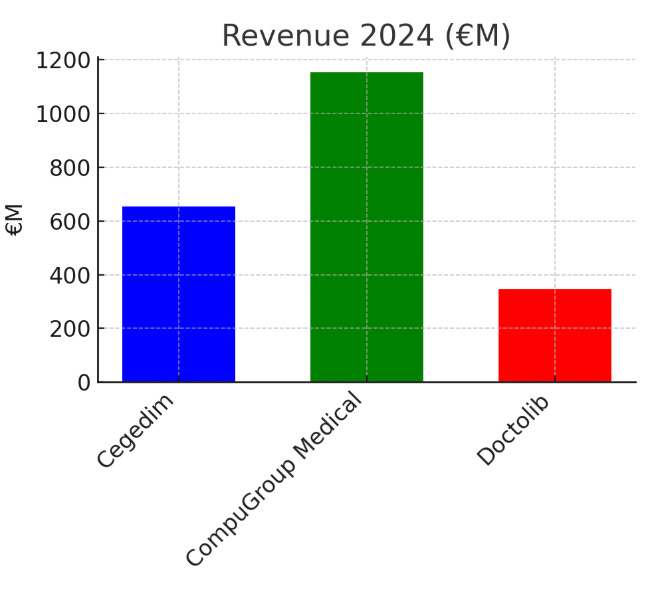

Founders often report 6–8 years on average to reach profitability; many only IPO around year 12. Doctolib was founded in 2013. It therefore took 13 years to reach profitability, which is significantly longer than a typical SaaS, even though it aligns with many high-growth health-tech peers. Doctolib’s revenue still trails those of its peers Cegedim (€654.5 million in 2024, up +6.3% vs. 2023) and CompuGroup Medical (€1,154.0 million in 2024, — 3% vs. 2023 (€1,187.7 million).

To be fair, the comparison is not entirely “iso” because Cegedim and CompuGroup Medical have large portfolios of different SaaS solutions. Cegedim, for example, has media solutions and cybersecurity solutions. However, I think the comparison still matters because it tells a lot about the industry Doctolib is in, an industry where players have to do a lot of different things in hopes of achieving profitability. And even when profitability is achieved, the net margin can be extremely thin.

In 2024, Cegedim recorded a -2.2% net margin (– 14.7 M€ on 654.5 M€ of revenue), despite a healthy 18.9% EBITDA margin. CompuGroup achieved roughly a 2.9% net margin in 2024 (≈ 33.6 M€ net profit on 1,154 M€ revenues). While positive, this sits below typical software and programming benchmarks (net margins around 14% on average) and below high-growth SaaS peers.

The reasons healthcare IT SaaS have low margins reside in the need to invest a lot of money on R&D and compliance costs, especially when you must interoperate with hospitals, clinics, and insurers. In some cases, you even have to deliver customized implementations, thus diluting economies of scale. And don’t forget the pricing pressure from public health systems and large group purchasers.

Fortunately for Doctolib, they can achieve economies of scale because of an “out-of-the-box” model: the same platform is replicated from one client to another, onboarding and implementation are done via standard workflows, and professionals (offices, clinics) subscribe online via packaged formulas. Also, so far, they do not have to deal with the strong pricing pressures of public healthcare systems or large buyers, such as some hospital software publishers. But this last point might not be true in the long term because for Doctolib to survive, they will have to enter public hospitals on a massive scale. More on that later.

In France, 50 million patients use Doctolib. France has approximately 68 million people, so this points to a saturation in the French market that did not translate into stellar profits. Doctolib is entering other markets in the EU, and that’s good. The problem is that these countries often have their own version of Doctolib already operating. Doctolib, the outsider, will have to fight tooth and nail to gain market share. 13 years after its creation, it is fair to say that Doctolib has lost the effect of surprise. Does all this mean that Doctolib is doomed? Not necessarily.

Doctolib will have to expand the set of solutions they propose. It’s the inevitable next step to grow and dethrone competitors like Cegedim, which are old (founded in 1969). Doctolib’s edge is the technological one. It comes from a modern, user-centric web and mobile experiences. Doctolib can ship features faster and better than incumbents. Doctolib should maintain that tech edge at all costs.

For the purpose of this article, I went on the Cegedim website and looked at all the solutions they proposed. It’s a lot. They are deeply entrenched. Dethroning them in the healthcare space, where government, decade-old relationships, and resistance to IT transformation are rampant, will not be easy.

But I also noticed something. The overall landing page seems dated. When I tried to look at the solutions in the English version of the page, I couldn’t scroll down. Look at the GIF. In the English version, nothing moves, but I was actually trying to scroll down.

And that’s just the landing page. Now imagine how dated and not user-friendly the SaaS solutions they propose to hospitals, clinics, and others should be. Their weakness is clearly in technology, and Doctolib can exploit that. The first step, which is the hardest one, will be to find an entry point, a breach. It is totally possible.

It’s worth noting that Doctolib’s path to profitability was lengthened by its aggressive R&D spending: the company earmarked €92 million for innovation in 2023 (a 24 % increase over 2022) and maintained a €100 million R&D budget in 2024 — roughly 29 % of its €348 million ARR — underscoring a deliberate choice to prioritize long-term tech leadership over short-term margins.

Those investments have fueled AI-driven features like the Consultation Assistant — which has already supported over 1.5 million patient encounters by automating note-taking and streamlining workflows — and the October 2024 launch of an auto-dossier population tool, further cementing Doctolib’s competitive moat by embedding advanced intelligence deeply into its platform.

By reaching the level of revenue they’ve reached and delivering a stellar customer experience (83% of general practitioners and pediatricians say the service saves them time and improves their daily workflow), Doctolib has built the credibility necessary to disrupt incumbents.

The fight won’t be easy, though. Let’s wait and see.